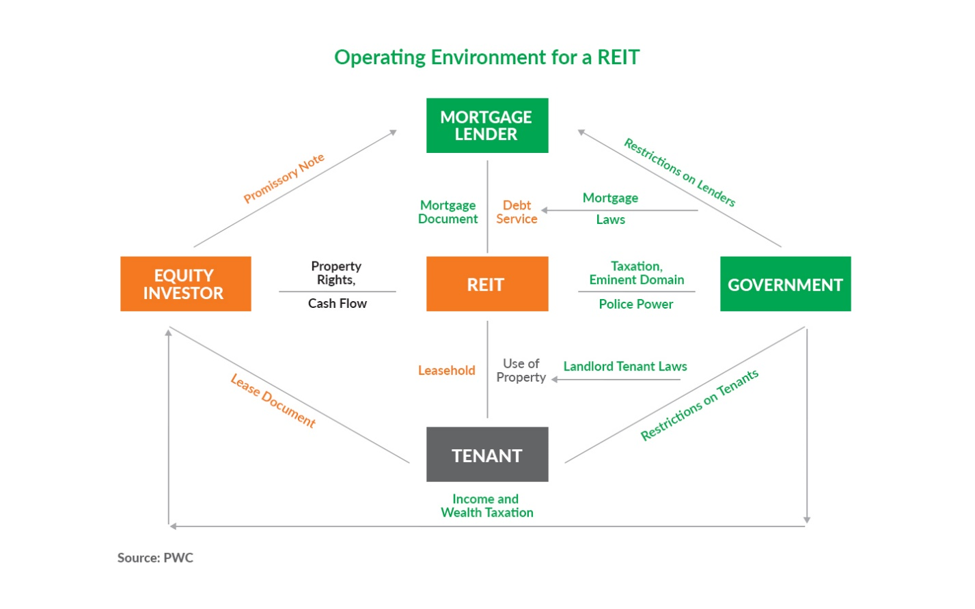

In part I of this article, we discussed Real Estate Investment Trust (REITs) as a fast emerging opportunity for real estate developers, builders, and investors alike (read more Part I). In a country like Pakistan, where financing institutions are highly risk-averse, especially when it comes to builder finance, REITs can offer an alternative and share the burden of existing financial systems. However, the existing regulations in the country are not conducive to the issuance of REITs.

The Securities Exchange Commission of Pakistan (SECP) introduced the first REITs framework in 2008 and made amendments in the subsequent years in order to promote them. For instance, in 2010 and 2015, requirements such as eligibility criteria in terms of capital outlay, size of the scheme, grace period of mandatory listing, and units held by a single investor were relaxed.

However, stakeholders believe that there are still several other regulatory and tax-related challenges that need addressing. For one, there should be no advance tax on REITs. Since REITs distribute at least 90 percent of their income as dividends, they should be exempted from advance tax under Clause 99 of the Second Schedule, Income Tax Ordinance.

Secondly, there is the issue of multiplicity in taxation. Both the federal and provincial governments are collecting taxes even though housing comes under the provincial domain.

Similarly, collection of capital value, stamp duties, and registration taxes when land is transferred from sponsors to the REIT structure makes little sense, since it is a non-cash transaction and is merely a paper-work. This puts REITs structure at a disadvantage in the real estate sector as compared to other real estate developers operating as a proprietorship, partnership, or limited company.

Moreover, the taxation burden on REITs is considerably higher as compared to that collected from market-based real estate transactions. The market-based transactions are reported at book value based on the valuation table of the FBR—which though have been rationalized— and are often lower than the actual market values. REIT, on the other hand, records transactions at the actual value, and as a result, pays substantially higher taxes (this applies to the advance tax as well since the valuation on which tax is collected differs between REIT and real estate transactions in the market).

This is a major deterrent and an out-of-pocket expense that the owner has to pay upfront before the issuance even begins. In a developmental REIT, the owner or builder, hoping to finance the construction of property through the issuance, has to pay taxes without realizing any cash.

From the builder’s perspective, REIT disclosure requirements are fairly high. All transactions within REIT are required to be documented and based on declared money which in the real estate business may not be easy to accomplish as the sector remains informal. It is also argued that the ground reality is very different and that buyers may not have enough white money to actually make REITs a success—unless disclosure requirements are relaxed.

Moreover, particularly for small and medium-sized builders, the documentation process is lengthy, cumbersome and costly. The lack of capacity within real estate builders to meet many of the paperwork requirements continues to deter them from seeking any form of formal financing, and REITs are no exception.

Also, there are certain unavoidable costs of listing REITs on the stock exchange which makes it financially burdensome. These may include undertaking property valuations, fulfilling legal due-diligence, obtaining credit rating, and appointing service providers.

There are also leveraging issues. For instance, the SECP does not allow borrowing in the REIT structure which means all projects have to be developed on equity of investors and money raised by floating the share. This is a big impediment, especially for larger projects, because it limits the builders’ access to a restricted pool of funds. A healthy debt-to-equity ratio is important for long-term commercial viability. Relaxing all these constraints is crucial for the development of the real estate sector and the financial system. Moreover, for REITs to be accessible to the average-sized builder, the listing requirements (issuance minimum and project cost) will have to be lowered from its current levels.